Federal income tax is a progressive taxation system that requires employers to withhold a percentage of employee wages based on income brackets, filing status, and allowances claimed on Form W-4.

For HR managers in tech, finance, and startup environments, understanding federal income tax withholding is crucial for accurate payroll processing, maintaining compliance, and supporting employee financial wellness. Proper tax management protects your organization from costly penalties while ensuring your team members receive accurate paychecks and tax documents.

With remote work expanding across state lines and tax regulations evolving annually, mastering federal income tax withholding has become a competitive advantage for organizations seeking to attract and retain top talent while minimizing compliance risks.

The system operates through tax brackets, where higher earners pay progressively higher rates on portions of their income. Your employees' taxable income determines which bracket applies, affecting their take-home pay and overall compensation satisfaction. Unlike state income tax which varies by location, federal rates remain consistent across all states.

Understanding how federal income tax impacts your team becomes crucial when structuring competitive compensation packages. Employees can reduce their tax burden through various tax credit opportunities and pre-tax deductions, making benefits like retirement contributions and health savings accounts more valuable than simple salary increases.

For remote teams spanning multiple states, federal tax obligations remain constant while state requirements vary significantly. This consistency simplifies payroll management when hiring across state lines, though you'll still need to navigate different state income tax requirements for each employee's location.

How federal income tax work?

The federal income tax operates as a progressive tax system where your tax burden increases with higher income levels. The Internal Revenue Service (IRS) collects these taxes based on the income you earn during each tax year, which runs from January 1 to December 31.

Your marginal tax rate represents the percentage applied to your last dollar of income, while your effective tax rate shows your overall tax burden as a percentage of total income. These rates differ significantly and impact your take-home pay calculations for employee compensation planning.

Tax brackets: Income tax rates range from 10% to 37% based on filing status and income levels

Deductions: Tax deductions reduce your taxable income, including standard or itemized options

Credits: Direct reductions like the child tax credit lower your actual tax owed dollar-for-dollar

When filing your annual tax return, you'll calculate your total tax liability and compare it against taxes already withheld from paychecks throughout the year.

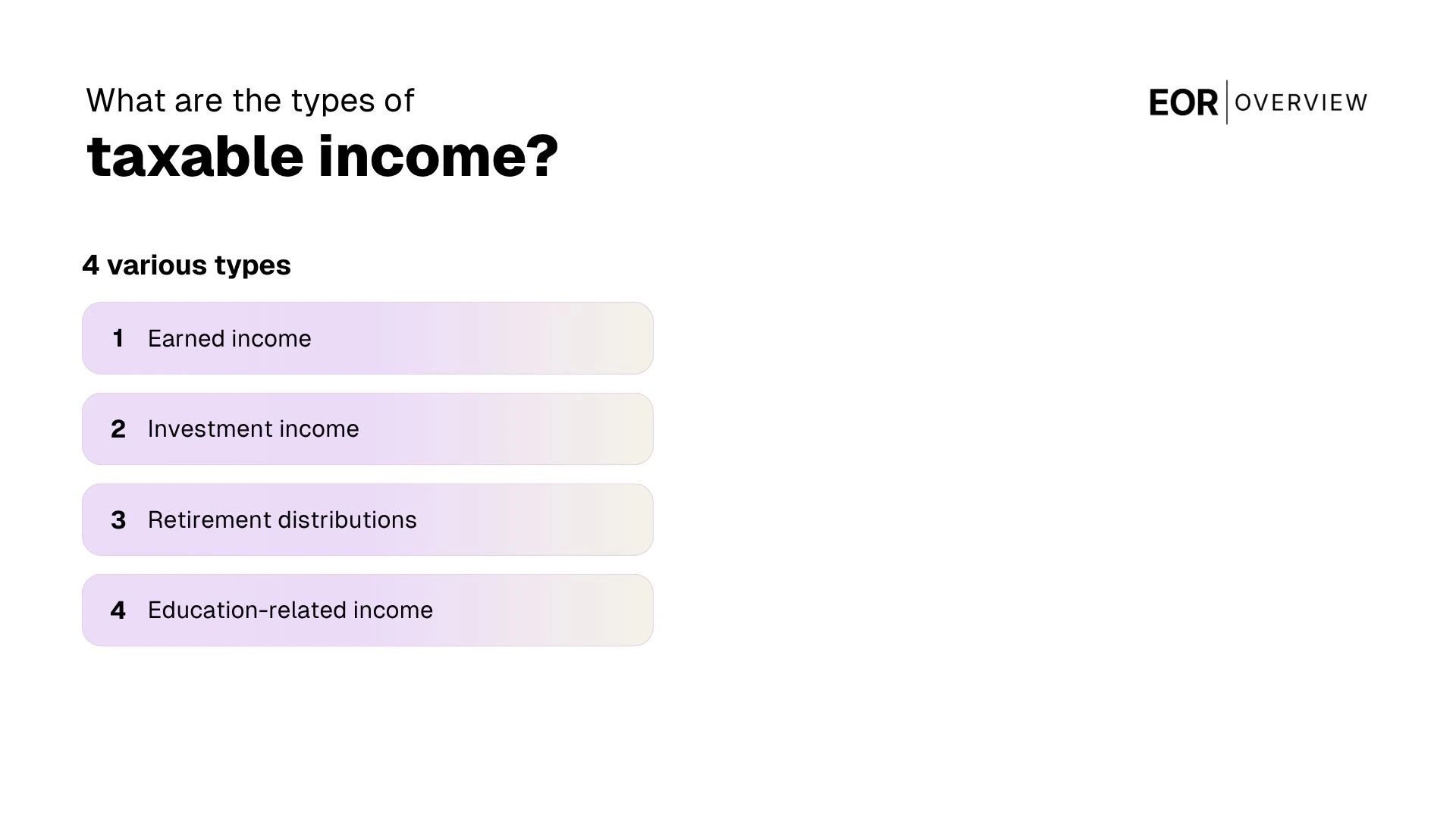

What are the types of taxable income?

Understanding the various types of taxable income helps you accurately calculate what you owe and identify opportunities to reduce your tax liability. The federal tax system applies seven tax brackets to different income categories, and your marginal tax bracket determines the rate on your last dollar earned.

When filing your return, you'll report earned income, investment income, and other taxable sources. Your net income after deductions determines your final tax obligation and potential refund amount.

Earned income: Wages, salaries, tips, and self-employment earnings that may qualify for the earned income tax credit if you meet income thresholds.

Investment income: Dividends, interest, capital gains, and rental income taxed at different rates depending on holding periods and income levels.

Retirement distributions: 401(k) withdrawals, IRA distributions, and pension payments that increase your taxable income when you pay taxes on previously deferred amounts.

Education-related income: Scholarships, grants, and loan forgiveness that may be offset by credits like the american opportunity tax credit for qualifying education expenses.

Gross income vs net income

Understanding the difference between gross income and net income is crucial for accurate tax filing and calculating your total tax bill. Gross income represents your total earnings before any deductions, while net income is what remains after subtracting allowable deductions from your gross income.

For 2024 tax purposes, your gross income includes wages, salaries, bonuses, freelance payments, investment returns, and other taxable income sources. This figure determines your initial tax bracket under the progressive tax system, where higher income levels face higher tax rates.

Net income becomes the foundation for your actual tax calculation in tax year 2024. By claiming standard or itemized deductions, you can reduce the amount of tax owed on your gross income. Single filers can claim a standard deduction of $14,600 for 2024, which directly lowers their taxable income and overall tax liability.

Who pays the income tax?

Most Americans who earn income are required to pay federal income taxes, making this system the primary source of revenue for the federal government. Your federal income tax liability depends on several factors including your total earnings, filing status, and available deductions.

The tax system applies to different types of income including wages, salaries, bonuses, freelance earnings, investment returns, and business profits. As an HR or hiring manager, you'll encounter employees with varying income sources, from traditional W-2 wages to stock options and contractor payments.

Individual taxpayers calculate their taxes on their income after subtracting the standard deduction or itemized deductions. For 2024, the standard deduction provides significant tax relief, reducing the taxable income base for millions of workers across tech, finance, and startup sectors.

Certain individuals are exempt from filing requirements, including those whose income falls below specific thresholds based on age and filing status. However, most full-time employees in your organization will have federal tax obligations that require proper withholding and documentation throughout the year.

Why do we pay income taxes?

Federal income taxes serve as the primary source of revenue for the United States government, funding essential services like national defense, infrastructure, and social programs. When you receive income from employment, investments, or business activities, the government requires a portion to support these collective needs that benefit society as a whole.

The tax system operates on a progressive structure, meaning higher earners pay proportionally more than those with lower incomes. Your adjusted gross income determines which tax bracket applies to different portions of your earnings. This includes wages, capital gains from investments, and other income sources that affect your tax liability across a wide range of income levels.

Beyond individual contributions, corporate income taxes from businesses also fund government operations. The tax code includes various mechanisms like refundable tax credits to provide relief for specific circumstances, and numerous strategies exist to help taxpayers legally reduce your federal income tax burden through deductions, credits, and proper planning.

What are income taxes used for?

Federal income taxes serve as the primary funding mechanism for essential government operations and public services. When your taxable income increases and you're required to pay federal income taxes, those funds directly support critical infrastructure, national defense, social programs, and administrative functions that keep the country running.

Federal tax revenue supports government operations, social security programs, medicare and medicaid, national defense, infrastructure development, and education initiatives. These categories represent the core areas where your tax contributions make a direct impact. These funding categories are detailed below.

Government operations: Administrative costs, federal employee salaries, and day-to-day operational expenses across all government agencies and departments.

Social security programs: Retirement benefits, disability insurance, and survivor benefits that provide financial security for millions of Americans.

Medicare and medicaid: Healthcare coverage for seniors, low-income individuals, and families who qualify for government-assisted medical care.

National defense: Military operations, equipment, personnel, and homeland security measures that protect national interests.

Infrastructure development: Roads, bridges, airports, and public transportation systems that support economic growth and commerce.

Education initiatives: Federal funding for schools, student loan programs, and educational research that strengthens the nation's workforce.

For HR professionals managing payroll in 2023, understanding how the amount your employer withholds from employee paychecks contributes to these services helps explain the value proposition to your team. Whether processing salary payments or dividend distributions, proper tax withholding ensures employees contribute their fair share to these essential public services.

Filing federal income taxes

Filing federal income taxes requires understanding which Form 1040 version applies to your situation. Most taxpayers use the standard Form 1040, while seniors aged 65 and older can opt for Form 1040-SR, which features larger print and simplified formatting. Your adjusted gross income (AGI) determines eligibility for various deductions and credits throughout the filing process.

The federal income tax system serves as the largest source of revenue for the U.S. government, making accurate filing essential for both individual compliance and national operations. Married couples filing jointly often benefit from lower tax brackets and higher income limits for deductions, though they must report combined income from both spouses on a single return.

Understanding the difference between refundable and nonrefundable credits significantly impacts your tax outcome. While nonrefundable credits can only reduce your tax liability to zero, refundable credits may help you get a refund even if you owe no taxes. Remember that federal filing requirements exist separately from state taxes, and each state maintains its own filing deadlines and income limit thresholds for required submissions.

Understanding federal income tax brackets

Federal income tax brackets operate on a progressive system where your tax rate increases as your income rises. Understanding these brackets helps HR managers and hiring managers communicate compensation packages more effectively and ensures employees complete their form w-4 accurately to optimize their paycheck withholdings.

The bracket system applies to all types of taxes at the federal level, but your specific rate depends on your filing status and total taxable income. When an employee earns income that crosses multiple brackets, only the portion within each bracket gets taxed at that rate, not their entire salary.

Your tax calculation includes income from wages, bonuses, and other compensation sources. Employees in lower brackets naturally pay less in federal taxes, while those in higher brackets face increased rates on income above specific thresholds. This progressive structure means that strategic compensation planning can help optimize both employer costs and employee take-home pay.

Marginal tax rate vs. effective tax rate

Understanding the difference between marginal and effective tax rates is crucial for HR professionals managing payroll and employee compensation strategies. Your marginal tax rate represents the percentage of tax applied to your last dollar of income, while your effective tax rate is the overall percentage of your total income paid in taxes.

The marginal rate follows a progressive system where different tax brackets levy varying percentages on income ranges. For example, a tech startup employee earning $85,000 might fall into the 22% marginal bracket, but this doesn't mean their entire income faces this rate. Only the income above the previous bracket threshold gets taxed at 22%.

The effective tax rate provides a more accurate picture of an employee's actual tax burden. This rate accounts for the progressive nature of federal taxation, where low-income portions of salary face lower rates. Finance professionals often use effective rates when calculating take-home pay projections and evaluating the true cost of compensation packages, as tax credits can directly reduce the amount owed and lower the effective rate significantly.

How do tax brackets work?

The federal tax system uses a progressive bracket structure where different portions of your income are taxed at increasing rates. Each earner pays the same rate on income within each bracket, regardless of their total earnings.

Your income moves through brackets sequentially, with only the amount in each bracket taxed at that specific rate. For example, if you earn $60,000, the first portion is taxed at 10%, the next portion at 12%, and so on until you reach your total income.

Marginal tax rate: The rate applied to your last dollar of taxable income, which determines your highest bracket.

Effective tax rate: Your total tax divided by total income, always lower than your marginal rate due to the bracket system.

Taxable income calculation: Your gross income minus deductions, which may include unemployment compensation or other sources.

Remember that tax-exempt income like certain municipal bonds and the portion of the credit from qualified retirement contributions don't count toward your bracket calculation, while tax-free employer benefits can significantly impact your effective rate.

How to reduce your taxes?

Strategic tax reduction requires a comprehensive understanding of available deductions and credits that align with your business operations. For HR managers and hiring professionals, the complexity of federal income tax planning increases when managing remote teams across multiple jurisdictions, especially when dealing with foreign entities or international contractors.

The most effective approach involves maximizing legitimate business deductions while ensuring compliance with current tax regulations. Employee-related expenses, including recruitment costs, training programs, and remote work equipment, can significantly impact your tax liability. Tax rates range from 10 percent to 37 percent for individuals, while corporate rates vary based on business structure and income levels.

Remote hiring presents unique opportunities for tax optimization through strategic workforce planning. Companies can leverage home office deductions, technology expenses, and professional development costs to reduce their overall tax burden. However, income from international sources may be taxed differently, requiring careful documentation and compliance with both domestic and foreign tax obligations.

Your ability to minimize taxes depends on proactive planning and accurate record-keeping throughout the year. Working with qualified tax professionals ensures you capture all available deductions while maintaining compliance with evolving regulations in the remote work landscape.

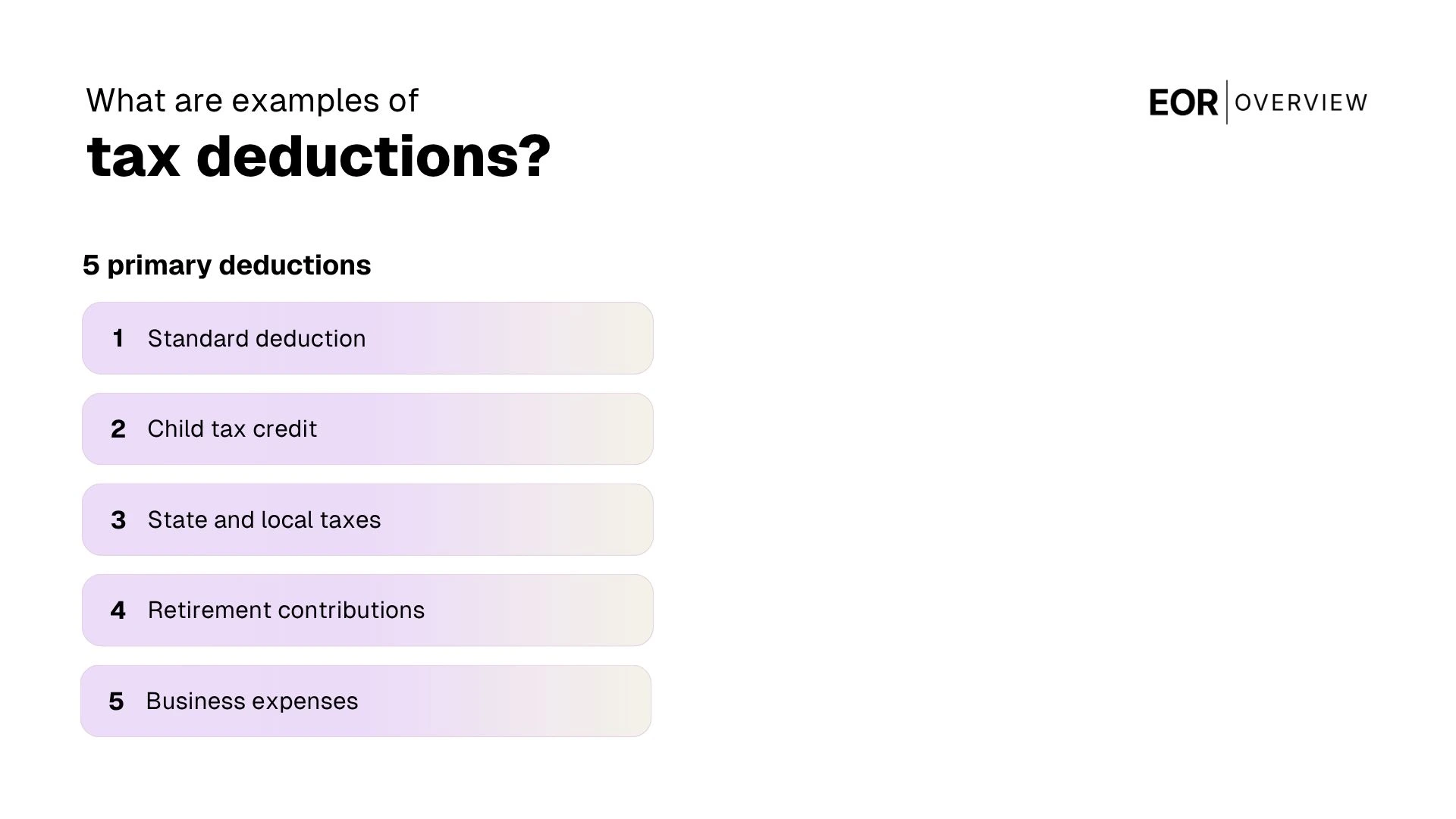

What are examples of tax deductions?

Tax deductions reduce the amount of income that taxpayers pay federal taxes on, directly lowering their overall tax burden. Understanding common deductions helps HR and hiring managers better support employees during tax season and when structuring compensation packages.

The primary deductions include standard deduction, itemized deductions, business expenses, retirement contributions, and dependent-related deductions. These deductions correspond to different aspects of taxpayers' financial situations and vary based on filing status and location.

These deductions are listed in detail below.

Standard deduction: A fixed amount that reduces taxable income without requiring documentation, varying by filing status and updated annually by the IRS.

Child tax credit: Parents can claim up to $2,000 per qualifying child, with families receiving additional benefits for one child or multiple dependents under age 17.

State and local taxes: Taxpayers can deduct state income taxes, property taxes, and sales taxes up to $10,000, though residents of states like South Dakota with no state income tax may focus on property and sales tax deductions.

Retirement contributions: Traditional IRA and 401(k) contributions reduce current taxable income while building long-term savings.

Business expenses: Self-employed individuals and contractors can deduct legitimate business costs including home office expenses, equipment, and professional development.

State income tax vs. Federal income tax

Understanding how taxes work requires recognizing the fundamental difference between state and federal tax systems. Income tax is a tax levied on earnings, but the structure varies significantly between federal and state levels within the u.s. While federal income tax applies uniformly across all states with standardized brackets and deductions, state income tax policies differ dramatically from one jurisdiction to another.

Federal income tax operates under a progressive system with rates ranging from 10% to 37% based on income levels and filing status. This system remains consistent whether you're hiring talent in California or Wyoming. State income tax, however, presents a more complex landscape for HR managers and hiring teams to navigate.

Seven states, including Wyoming, impose no state income tax on wages, creating significant advantages for both employers and employees. This disparity affects compensation strategies, talent acquisition costs, and employee retention across different markets. For tech startups and finance companies expanding their remote workforce, understanding these variations becomes crucial for competitive positioning and budget planning.

Individual vs. Other federal income taxes

Federal income tax structures vary significantly depending on the taxpayer type, creating distinct compliance requirements for HR managers overseeing payroll operations. Individual federal income tax applies to employees' wages, salaries, and other compensation through a progressive rate system ranging from 10% to 37% based on income brackets.

Corporate federal income tax operates under a flat 21% rate for C-corporations, while pass-through entities like S-corporations and partnerships transfer tax liability directly to individual owners. This distinction becomes crucial when structuring compensation packages for executives and equity participants in tech startups and finance companies.

Self-employment tax adds another layer for independent contractors, requiring an additional 15.3% for Social Security and Medicare contributions. HR teams must carefully classify workers to ensure proper tax withholding and avoid compliance issues with the IRS.

Understanding these tax categories enables hiring managers to make informed decisions about contractor versus employee classifications, equity compensation timing, and benefits structuring that optimize both company costs and employee take-home pay in competitive talent markets.

Does Social Security count as income for tax purposes?

Social security benefits can be subject to federal income tax depending on your combined income and filing status. The IRS uses a specific formula that includes your adjusted gross income, nontaxable interest, and half of your social security benefits to determine taxability.

For individual filers, social security becomes taxable when combined income exceeds $25,000, with up to 50% of benefits taxable between $25,000-$34,000, and up to 85% taxable above $34,000. Married couples filing jointly face taxation when combined income surpasses $32,000, with the same percentage thresholds applying at $32,000-$44,000 and above $44,000 respectively.

This taxation particularly affects high-earning professionals in tech and finance who may have substantial retirement accounts or continued consulting income. HR managers should consider this when designing retirement planning benefits, as employees transitioning to social security may face unexpected tax burdens that impact their overall compensation strategy.

When is federal income tax due?

Federal income tax returns are typically due on April 15th of each year for the previous tax year. This deadline applies to both individual taxpayers and businesses filing their annual returns. However, when April 15th falls on a weekend or federal holiday, the deadline automatically extends to the next business day.

For HR managers and hiring teams, understanding these deadlines becomes crucial when managing payroll tax obligations and employee tax documents. Companies must distribute W-2 forms to employees by January 31st and file copies with the Social Security Administration by the same date. This timing ensures employees have adequate time to prepare their personal returns before the April deadline.

Missing federal tax deadlines can result in significant penalties and interest charges. The failure-to-file penalty alone can reach up to 25% of unpaid taxes, making timely compliance essential for both individuals and businesses.

Taxpayers who need additional time can request an automatic six-month extension by filing Form 4868 before the original due date. This extension moves the filing deadline to October 15th, though any taxes owed must still be paid by the original April deadline to avoid interest and penalties.